Learning Outcomes

This article explains how to apply core time value of money techniques to typical CFA Level 1 problem types. It shows how to translate verbal descriptions of investments, loans, and securities into clearly defined cash flow timelines and TVM variables (PV, FV, r, N, PMT). The article explains how to compute present and future values for single sums, level annuities, and perpetuities using both formulas and financial calculators, and how to adjust inputs when compounding is non‑annual. It details how to distinguish ordinary annuities from annuities due, determine which formula structure to use, and verify results through quick reasonableness checks. It also examines how interest rates function as required returns, discount rates, and opportunity costs, and how to convert between stated rates, periodic rates, and effective annual rates (EAR). Finally, the article reviews methods for solving for unknown variables—such as the discount rate, number of periods, or payment amount—and highlights common exam traps involving sign conventions, timing of cash flows, and inconsistent treatment of r and N.

CFA Level 1 Syllabus

For the CFA Level 1 exam, you are expected to understand and apply the time value of money, with a focus on the following syllabus points:

- Defining and interpreting interest rates as required returns, discount rates, or opportunity costs

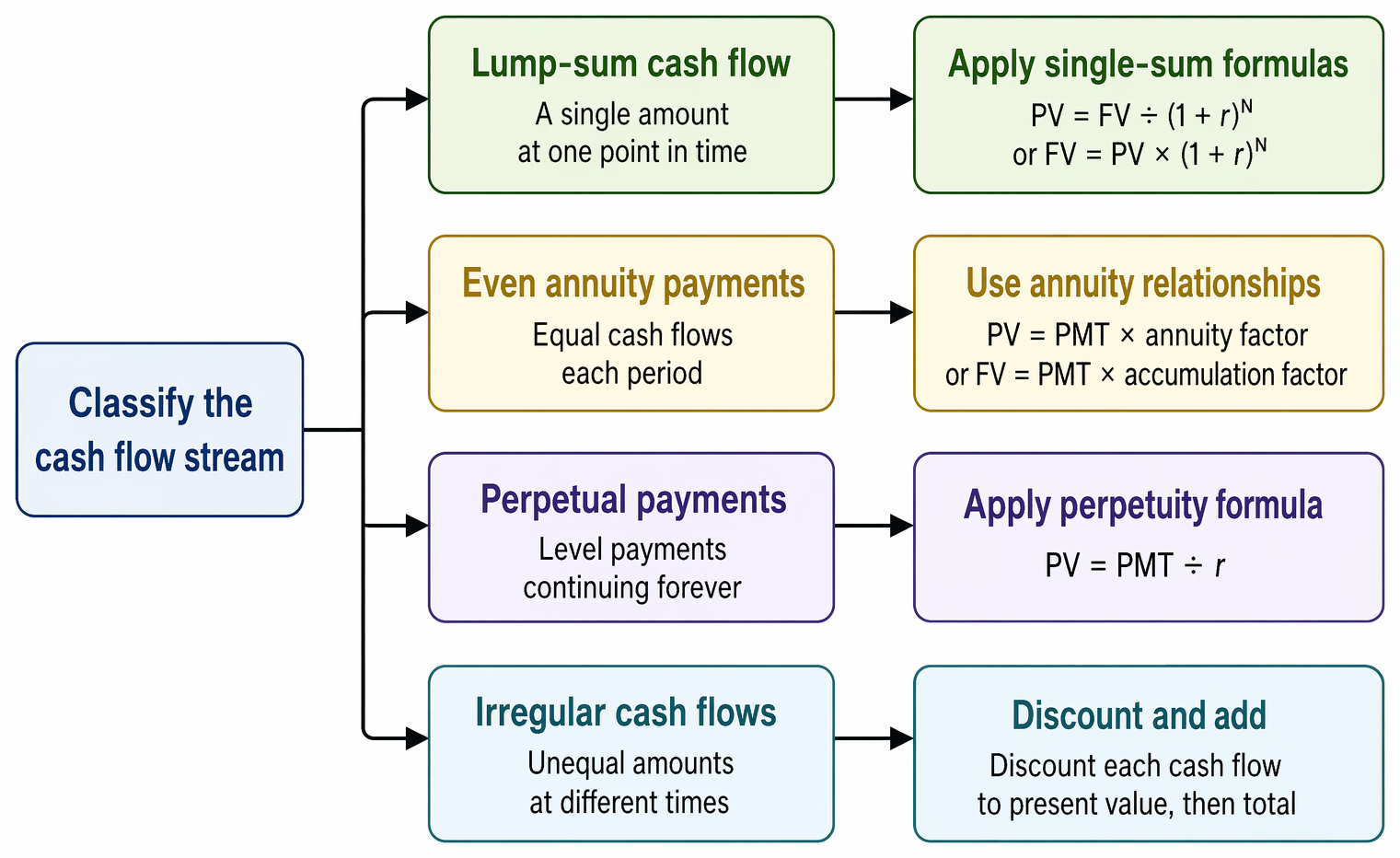

- Calculating present value (PV) and future value (FV) for single sums, annuities, perpetuities, and series of unequal cash flows

- Recognizing and applying formulas for discounting and compounding

- Solving for unknowns: rates, periods, or payment amounts in TVM problems

- Distinguishing between ordinary annuities and annuities due

- Identifying the impact of compounding frequency and recognizing the difference between stated, periodic, and effective rates

Test Your Knowledge

Attempt these questions before reading this article. If you find some difficult or cannot remember the answers, look more closely at that area during your revision.

- What is the present value of $10,000 to be received in four years, discounted at an annual rate of 6% compounded annually?

- Which formula gives the future value of an ordinary annuity after periods at rate per period?

- True or false? If interest compounds semiannually, the stated annual rate equals the effective annual rate (EAR).

- What is the present value of a perpetuity of $500 per year if the appropriate discount rate is 8%?

Introduction

The time value of money (TVM) forms the basis of finance. Gaining command of TVM enables you to compare cash flows spread across time—whether for bonds, loans, investments, or retirement savings. Discounting brings future amounts back to their value today; compounding pushes present values forward in time. Annuities and perpetuities extend the concept to repeated payments.

Key Term: time value of money

The principle that money received (or paid) at different times is not equivalent; a dollar now is worth more than a dollar in the future due to its earning capacity.

Complications arise: cash flows may differ, interest may compound more frequently than annually, or annuities might start at different times. This article explains each concept, presents the primary formulas, and demonstrates exam-relevant approaches.

The Components of Interest Rates

Interest rates are the "exchange rate" between present and future cash. For TVM calculations, interest rates serve as a discount (bringing cash flows to present value), as a required return, or as the opportunity cost of capital.

Key Term: interest rate

The rate of return expressing the relationship between differently dated cash flows, used as a discount rate, required return, or opportunity cost.

Interest rates in calculations may be stated annually, but compounding can occur more frequently (quarterly, monthly), and the distinction between the stated, periodic, and effective rates is critical for the exam.

Discounting and Present Value

Discounting means calculating today's equivalent value for a sum to be received in the future.

Key Term: present value (PV)

The value today of a future cash flow, discounted at a specified rate.

The basic formula for the present value of a single cash flow is:

Where:

- = future value

- = interest rate per period

- = number of periods

The same formula applies for discounting annually. For non-annual compounding, divide the interest rate by the number of periods per year and multiply accordingly.

Worked Example 1.1

You will receive $15,000 in three years, and the discount rate is 7%, compounded annually. What is the present value?

Answer:

Exam Warning: Frequent exam errors include using the nominal (not periodic) rate, or failing to adjust N and r for compounding frequency.

Compounding and Future Value

Compounding projects money forward from today by adding earned interest to principal, period after period.

Key Term: future value (FV)

The amount an investment grows to after earning interest for N periods at rate r.

The standard formula for a single initial investment is:

Worked Example 1.2

Suppose you invest $5,000 at 5% annual interest compounded annually. What will it be worth in six years?

Answer:

When the compounding frequency increases (e.g., quarterly, monthly), use the periodic rate ( divided by number of periods per year) and total number of periods ( times periods per year).

ANNUITIES

An annuity is a series of equal cash flows paid or received at regular intervals.

Cash flow classification directs selection of single-sum, annuity, perpetuity, or separate discounting formulas in time value of money calculations.

Key Term: annuity

A finite sequence of level, equally spaced payments.

There are two types:

- Ordinary annuity: Payments occur at the end of each period (most common in exam questions).

- Annuity due: Payments occur at the beginning of each period.

The present value of an ordinary annuity is:

The future value of an ordinary annuity is:

Where:

- = payment per period

- = interest rate per period

- = number of payments

Worked Example 1.3

You deposit $2,000 at the end of each year into an account paying 4% annually. What will you have after 5 years?

Answer:

Revision Tip: Remember, for an annuity due (payments at the beginning of the period), multiply the ordinary annuity value by (1 + r).

PERPETUITIES

A perpetuity is a special case of an annuity with payments continuing forever.

Key Term: perpetuity

An infinite stream of level, equally spaced cash flows.

The present value of a perpetuity is:

Worked Example 1.4

A preferred stock pays an annual dividend of $4, with required return of 8%. What is the present value?

Answer:

Frequency of Compounding and Effective Rates

Interest may compound more than once a year—e.g., semiannually, quarterly, monthly.

- The periodic rate = stated annual rate / number of periods per year

- The effective annual rate (EAR) = the actual annual return, considering compounding

Key Term: effective annual rate (EAR)

The annualized equivalent rate accounting for intra-year compounding.

Where is the number of periods per year.

Worked Example 1.5

You invest $1,000 at a stated annual rate of 6%, compounding monthly. What is the effective annual rate (EAR)?

Answer:

The monthly periodic rate = 0.06 / 12 = 0.005

Exam Warning: Effective Rates

The exam often tests your ability to distinguish between the stated annual rate and EAR, especially with non-annual compounding.

Solving for Unknown Variables

You may be required to solve for:

- The interest rate , given , , and

- The number of periods

- The periodic payment in an annuity

Use formula rearrangement or a financial calculator.

Worked Example 1.6

You want to accumulate $20,000 in 8 years. If you deposit $2,000 at the end of each year, what annual rate must you earn?

Answer:

Solve for r using trial-and-error, algebra, or a calculator.

Common TVM Exam Mistakes

Exam Warning: Common Mistakes

- Failing to adjust r and N for non-annual compounding

- Mixing up annuity due and ordinary annuity

- Not using EAR when required

- Forgetting that present value and future value formulas are reciprocal

Summary

The time value of money underlies all valuation in finance. Present value and future value calculations allow you to compare and combine cash flows at different dates. Understanding annuities and perpetuities expands your ability to tackle real-world financial problems on the CFA exam. Always match compounding periods and rates, distinguish between stated rates and EAR, and carefully identify ordinary versus due annuities.

Key Point Checklist

This article has covered the following key knowledge points:

- Define and interpret interest rates as discount rates, required returns, and opportunity cost

- Calculate present and future values for single sums, annuities, and perpetuities

- Recognize when to apply discounting and compounding formulas

- Calculate effective annual rates and adjust for compounding frequency

- Distinguish between ordinary annuities and annuities due

- Solve for unknown rates, periods, or payment amounts in TVM problems

- Avoid common mistakes in TVM problems on the CFA exam

Key Terms and Concepts

- time value of money

- interest rate

- present value (PV)

- future value (FV)

- annuity

- perpetuity

- effective annual rate (EAR)